Contesting Taxes on Agribusiness Facilities

Over the last year, Compeer Financial Appraisers have fielded calls from several ag-business owners staring at their tax bills in disbelief, asking “How can I possibly owe that much in property taxes when I paid so much less last year?” There are two causes for an increase in taxes owed. The first reason for the tax hike is due to an increase in the tax rate to support public services. The second reason is attributed to a new assessment. In Illinois, real estate is generally assessed every four years (Illinois.gov). The Assessed value of a property is 1/3 of the estimated Fair Market Value (FMV) for the property and is the basis for the taxable value. A property is taxed at a percentage of the assessed value.

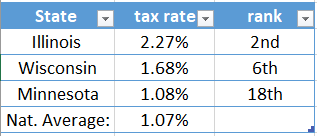

In the State of Illinois, property taxes have become an increasing concern for many small business owners and farmers. The State of Illinois has the second highest property tax rate, with an average effective tax rate of 2.27%. Wisconsin has the fourth highest rate at 1.68% of market value. Minnesota is ranked the 18th highest tax rate in the nation at 1.08%. (WalletHub)

In primarily rural counties, ag-business facilities tend to have high assessed values and therefore a higher tax basis, often times paying some of the highest taxes in the county. An over-assessed and over-taxed property can pose financial strain on a business in an already competitive market.

For most rural ag-business facilities, the assessment is determined by the county assessor. The assessor tracks trends in the market on a county-wide basis and conducts market analysis in an attempt to accurately assess a property for taxes. Historically, assessors have not been aggressive in the assessment of ag-business facilities such as local elevators. However, as schools and other public services have become increasingly desperate for funding, assessors have revisited assessments on properties which have generally not had significant changes to their assessments in quite some time. This trend toward assessing ag-business properties more aggressively, coupled with increasing tax rates, has caused many businesses to become shocked and frustrated with an enormous tax bill.

When it comes to specialized, high-end ag-business facilities, assessors may not always have the tools, resources, or expertise to select sales and market data which would be most comparable to a modern ag-business facility. In some circumstances, this can cause them to over-assess the property, leading to the higher taxes.

Our client, a local elevator, discovered this the hard way by uncovering their new tax bill for almost $200,000! The property owners recently constructed a new grain facility in a rural area with good access to rural highways. The site was located over four miles from the nearest town of just 1,700 people. The facility was a modern, state of the art grain elevator with approximately 3.5 million bushels of capacity. The elevator manager contacted Compeer Financial distressed by his tax bill and asked our appraisal team to analyze his taxes to see where he might be able to contest the assessment.

The Assessor had estimated the Fair Market Value of the facility and site at $8.4 million. After conducting an analysis on the property, we found that while the assessor had been reasonably accurate with the value of the improvements, they had missed the mark on the value of the land. The assessor had allocated about $1.2million of the $8.4 million Fair Market Value to the land, a value of almost $60,000 per acre on the 20 acres!

In researching the property, the appraiser learned that the subject property was located in “A-1” countywide zoning; however, the assessor was taxing the land as though it was commercial land. Under “A-1” zoning, grain facilities such as the subject are a permitted use as an agricultural facility. However, “commercial properties” are not a permitted use and should not be valued or taxed as such. Due to the zoning restrictions and the widespread availability of similar cropland parcels, the value of any land for use as site would likely carry similar value as the surrounding cropland.

At the time of the assignment, soils of similar productivity as the subject generally sold for approximately $13,000 in this area of the county, with taxes on cropland in the area around $50 per acre. Under this assumption, it could be reasonably concluded that the tax liability for the subject’s land would be $1,000 for the 20-acre tract.

Another way to view the subject’s land would be to analyze it as “commercial” land. Under this scenario, if the land were valued at $15,000 per acre, the taxes would amount to $350 per acre (assuming a 7% tax rate) or $7,000 per year. The current assessment had valued the land at $60,000 with taxes totaling roughly $28,000.

As an assignment result, we provided an opinion of Market Value for the land to the client, as well as additional documentation of our analysis. This additional documentation included information on similar properties, their tax liability, and how it compared to our client’s property. This provided enough documentation and analysis for our client and their attorney to feel comfortable contesting their taxes before a State Board of Review.

Although an appraisal cannot guarantee an outcome like this specific example, the Compeer Financial Appraisal Department will work to provide our clients with solid, reliable, and independent appraisals. We anticipate contesting taxes to be a growing trend within the ag-business sector and we are here to help find an equitable assessment.

https://www2.illinois.gov/rev/questionsandanswers/pages/317.aspx

https://wallethub.com/edu/states-with-the-highest-and-lowest-property-taxes/11585

Receive the latest industry insights directly. SIGN UP FOR APPRAISAL NEWSLETTER