Export Activity in the U.S. Dairy Market

Accounting for 9.7 percent of Compeer's outstanding volume, dairy makes up the second largest segment in Compeer's portfolio. A large portion of U.S. dairy is exported and, despite significant disruptions in trade throughout 2020, the United States exported nearly 2.4 million metric tons of dairy goods last year–a record-setting mark, according to data released by USDA's Foreign Agricultural Service (FAS). Michael Dykes, D.V.M., President and CEO of the International Dairy Foods Association (IDFA) issued the following statement:

"Last year was yet another banner year for U.S. dairy exports, a testament to the resilience, innovation, and growth of the U.S. dairy industry. While logistical issues challenged the industry in 2020 and some continue today, U.S. dairy exports maintained an accelerated pace throughout the year. Export volumes were boosted by 10 percent over 2019, setting an all-time record for export volumes in one year and pushing export values to more than $6 billion for the first time since 2014."

As the chart above shows, Mexico, which has traditionally been the biggest market for US dairy exports, showed a decline in 2020 versus the prior year. Mexico experienced dual setbacks of the recession and the pandemic that depressed dairy demand and imports throughout most of 2020. The few other countries in the top 20 export markets that did decline by volume all have known tariff and non-tariff barriers in place, on which IDFA has been advocating with the U.S. government.

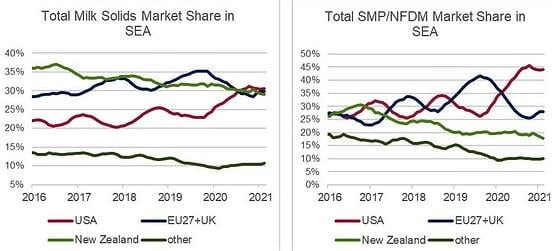

On the other hand, South East Asian (SEA) markets — China, Philippines, Indonesia, and Malaysia — saw increases between 35-50 percent in value over 2019, with correlating increases in volume to those markets, particularly milk solids, non-fat dried milk (NFDM), skim milk powder (SMP) and whey. The U.S. has steadily grown market share in SEA over the past year, overtaking New Zealand and the EU to become the largest market share holder in milk solids exports to the region, with a share of 31 percent (up from 23 percent in late 2019). In NFDM/SMP, the U.S. also leads with a market share of roughly 45 percent (up from 26 percent in late 2019).

Despite the increase in share, ongoing port issues remain a key obstacle for continuing the growth to SEA and China. While largely out of U.S. exporter control, importers may consider alternatives if they are unable to secure product when needed. This has the potential to limit further growth in the region if buyers decide that more consistent timing is worth paying a premium to get product from other suppliers. However, despite these challenges, U.S. dairy is well-positioned to continue growing exports to the region and capturing increased market share.

Whey exports also continue to show stellar performance. A major factor driving U.S. whey sales is the heavy Chinese purchasing to support efforts to rebuild a pig herd decimated by African Swine Fever. China reported that its herd had reached about 90 percent of normal levels at the end of November 2020. But given that pork output is still far short of demand and dry whey pricing levels suggest strong Chinese buying activity that should persist in 2021. U.S. whey shipments to China were up 111 percent year to date. U.S. suppliers have been able to grow volume and recapture market share in large part due to the retaliatory tariff exemption secured in 2019 and renewed in 2020 - 2021. China also topped all buyers for higher value whey products (WPC80+).

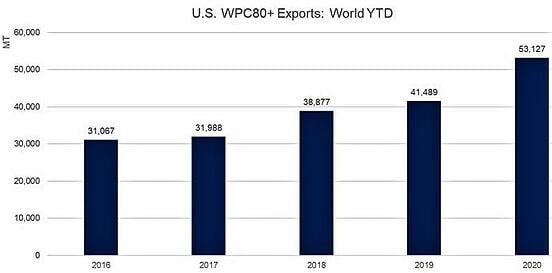

Reinforced by its nutritional reputation (a particular selling point over the pandemic period where we have seen populations focus more squarely than ever on healthy eating), U.S. WPC80+ exports continue to find more broad-based geographical growth, setting new records every single year since 2016. Last year set another record year. Exports to Japan (+27 percent), Southeast Asia (+73 percent), South Korea (+165 percent) and the EU+UK (+294 percent) all saw big gains in 2020.

Other dairy commodities (cheese, butter and lactose) also continue to show stellar export potential. For example, sales of U.S. cheese to international customers grew by 846 percent over the last 20 years, fueled by the excellent value offered by the U.S. dairy industry. In fact, as recently as 2019, a U.S. company (Rogue River Blue based in Oregon) was named the world’s best cheese at the 32nd annual World Cheese Awards. Butter output expanded by 50 percent over the last decade, however production has been stable in recent years due to stiff export competition from the EU and New Zealand. As for lactose, the United States has a long and proven track record as the world's largest lactose-exporting nation. Over two-thirds of U.S. lactose production annually is destined for overseas markets, reflecting the industry's strong export orientation, and strong global reputation for quality and performance.

Strong export performance significantly improves profitability prospects for Compeer clients. Expansion of dairy product exports to other regions of the globe provides significant geographic diversity for the industry, limiting impact of geopolitical disputes with a single export partner. As such, stability in export relationships benefits producers by providing a measure of stability in the marketplace.