Interest Rates and Building Costs Update

Today’s dynamic economy with an inflationary environment is challenging for producers. It may be a new year, but some producer concerns remain from last year. Like 2022, supply disruptions, demand and logistical headaches are keeping building costs high. Additionally, we wish we could say interest rates have come back down to historical lows and have helped offset the increases we have seen in building costs, but that is not the case.

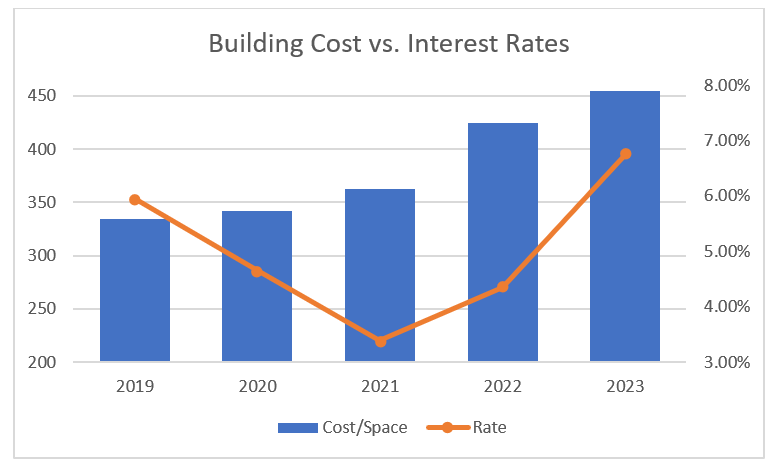

This time last year, we shared a five-year trend of building costs and interest rates. Now, unfortunately -- with updated figures reflecting 2022 actuals and 2023 projections -- it appears costs and interest rates continue to trend upward. The graphs below reflect this for a standard 2,400-head wean-to-finish barn with the following assumptions:

- 15-year term loan

- 85% loan financing

- Solid borrower credit

- Southern Minnesota and Northern Iowa cost averages

- Costs include all aspects except land

- Rates may vary based on specific loan pricing and products, young farmer program qualification and specific terms.

The interest rates shown were recorded in early January of each respective year and are based on above average borrower credit. Overall building costs for the site can change based on your equipment package, material quality and other factors, but we believe the trend captures what producers have been experiencing in the countryside.

There are a few key points to consider when analyzing the data. Since 2019, overall building costs have increased roughly 32%. Nearly a quarter (24%) of that occurred over the last two years alone. Conversely, during 2020 and 2021, interest rates decreased, offsetting the higher building costs..

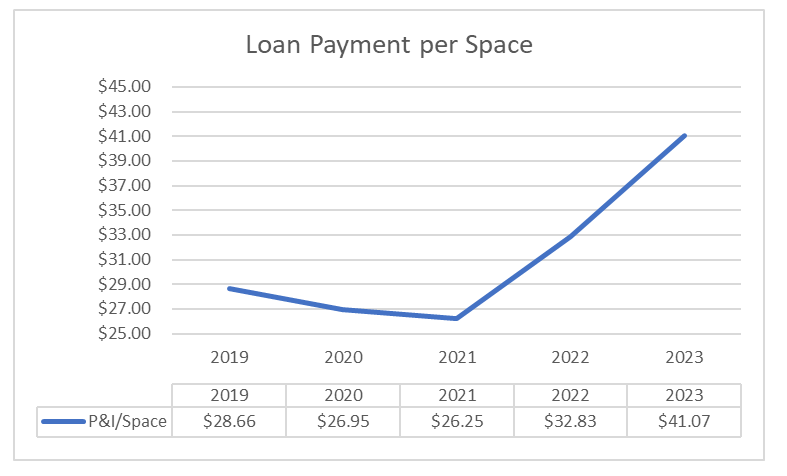

However, today we are seeing an increase in borrowing costs with certain rate products currently around the 6.5-7% range. During 2022, and now in 2023, both building costs and interest rates are working against the producer. Because of this, we have seen principal and interest per pig space drastically increase from 2021 to 2023. In order to keep the same loan payment per space as 2022, today you would need to have a down payment of roughly 32%. This is substantially higher than the 15% capitalization rate used in the 2022 scenario.

Considering the information above, it may be less appealing to build a new wean-to-finish barn. However, there are still some positives to note. Commercial fertilizer has also increased drastically, meaning producers are receiving a much greater value for their manure, helping offset the increase in debt cost. Based on this past fall’s N, P and K values, rough figures come out to $8-11 per space of commercial fertilizer savings. Additionally, hog barns have historically held their values exceptionally well. It is common for us to see existing barns appraise and sell for around the same price it took to originally construct them several years prior. This allows a producer to gradually build significant equity in a long-term asset, which in turn will help them grow their farming operation.

Finally, although we are seeing increased interest rates, from a historical perspective, these rates are not uncommon. Producers have been fortunate to benefit from low borrowing costs over the past 10-12 years. If history repeats itself, opportunities for refinancing to lower interest rates will happen once again.

In farming, there will always be obstacles to overcome. However, challenges can bring opportunity. When making borrowing decisions, producers should assess all angles of each opportunity to have the proper insight on how it will affect and improve their farm business now and for the future.

Dusty Compart is a Swine Lending Specialist, with Compeer Financial. For more insights from Dusty and the Compeer Swine Team, visit Compeer.com